If you have strong credit and want a fee-free loan with fast funding, this SoFi personal loan review will help you decide whether the lender lives up to its reputation. SoFi (short for Social Finance) has grown from a student-loan refinancer into a full-service digital bank, and its unsecured personal loans are among the most competitive on the market for well-qualified borrowers. The pitch is simple: no required origination fees, no late fees, no prepayment penalties, loans up to $100,000, and money in your account as soon as the same day.

But “no fees” and a high maximum don’t automatically make SoFi the right choice for everyone. Below we break down the rates, terms, costs, and eligibility so you know exactly what to expect before you apply.

In this article

| Loan amounts | $5,000 – $100,000 |

| APR range | Roughly 8.99% – 35.49% fixed (as of 2026 — confirm with a quote) |

| Repayment terms | 2 to 7 years |

| Fees | No required origination, late, or prepayment fees |

| Funding time | As fast as the same day |

| Best for / credit needed | Good-to-excellent credit (roughly 680+) |

SoFi personal loan rates & terms

SoFi offers fixed-rate personal loans from $5,000 to $100,000, one of the highest maximums in the industry. That high ceiling makes SoFi a natural fit for big-ticket needs like major home renovations, medical bills, or consolidating several high-interest credit cards into a single payment. The trade-off is the $5,000 floor: if you only need a couple thousand dollars, you’ll have to look elsewhere.

Repayment terms run from two to seven years. As of 2026, SoFi’s advertised APR range runs from the high single digits to roughly 35.49%, but rates move constantly and depend on your credit profile, income, loan amount, and term. Treat any published number as a starting point and confirm your actual rate with a quote.

One of SoFi’s most appealing features is that you can check your rate with a soft credit pull that does not affect your credit score. That lets you compare SoFi against other lenders risk-free before committing to a hard inquiry.

Rate discounts that add up

SoFi advertises stacking discounts that can meaningfully lower your APR. You can typically shave 0.25% off by enrolling in autopay, another 0.25% as a SoFi member benefit, and a further discount when you use the loan for debt consolidation and let SoFi pay your creditors directly. Those quarter-point discounts sound small, but over a five- or seven-year term they translate into real savings.

Fees & costs

This is where SoFi shines. There is no required origination fee, no late fee, and no prepayment penalty. Many competitors quietly skim 1% to 10% off the top as an origination fee, so a genuinely fee-free loan means you receive the full amount you borrow and can pay it off early without a penalty.

One nuance worth knowing: SoFi may let you opt into an origination fee (up to about 7%) in exchange for a lower interest rate. That can occasionally make sense if you plan to keep the loan for its full term, but for most borrowers the fee-free path is the cleaner deal. Read your offer carefully so you know which version you’re accepting.

Benefits & standout features

Beyond the no-fee structure, SoFi’s biggest strengths are speed and support. Approved borrowers can receive funds as fast as the same business day when the loan agreement is signed before the afternoon cutoff. The entire process is online, mobile-friendly, and famously smooth.

SoFi also allows co-borrowers, which can help you qualify or secure a better rate if your credit alone isn’t quite strong enough. And its unemployment protection program is a rare safety net among personal-loan lenders — a reassuring backstop if your income situation changes.

Who it’s for — and who should skip it

SoFi is best for borrowers with good-to-excellent credit (roughly 680 and up), stable income, and a need to borrow $5,000 or more. If that’s you, the combination of no fees, high loan limits, and member perks is hard to beat.

You should probably skip SoFi if you have fair or poor credit, need a very small loan under $5,000, or need same-day cash from a storefront. Borrowers with thin or damaged credit will likely find better approval odds with a lender like Upstart, which uses AI-based underwriting, or a fair-credit-friendly option such as Upgrade.

- No required origination, late, or prepayment fees

- High borrowing limit up to $100,000

- Same-day funding possible

- Stacking autopay and member rate discounts

- Unemployment protection and free financial planning

- $5,000 minimum shuts out small borrowers

- Best rates require strong credit and income

- No secured option for weaker-credit applicants

- Not ideal for fair-credit borrowers

What credit score do I need for a SoFi personal loan?

Does SoFi really charge no fees?

How fast can I get my money?

Can I use a co-borrower with SoFi?

The Bottom Line

This SoFi personal loan review lands on a clear conclusion: for borrowers with good-to-excellent credit who need to borrow $5,000 or more, SoFi is one of the strongest options available. The genuinely fee-free structure, $100,000 ceiling, fast funding, and member perks like unemployment protection make it a standout for debt consolidation and large planned expenses. Just remember that the best rates go to the strongest applicants, and the $5,000 minimum makes it a poor fit for tiny loans. Always compare a soft-pull quote from SoFi against at least one competitor — such as LightStream or Best Egg — before you commit. And if you’re borrowing to consolidate debt, pair the loan with a plan; our guide on investing versus paying off debt can help you decide where each extra dollar should go.

Read also

LightStream Personal Loan Review 2026: Is It Worth It?

Our LightStream personal loan review covers rates, terms, and its no-fee promise. Loans up to $100,000 with a Rate Beat…

Upstart Personal Loan Review 2026: Is It Worth It?

Our Upstart personal loan review covers its AI underwriting, rates, and fees. Loans from $1,000 with no strict minimum credit…

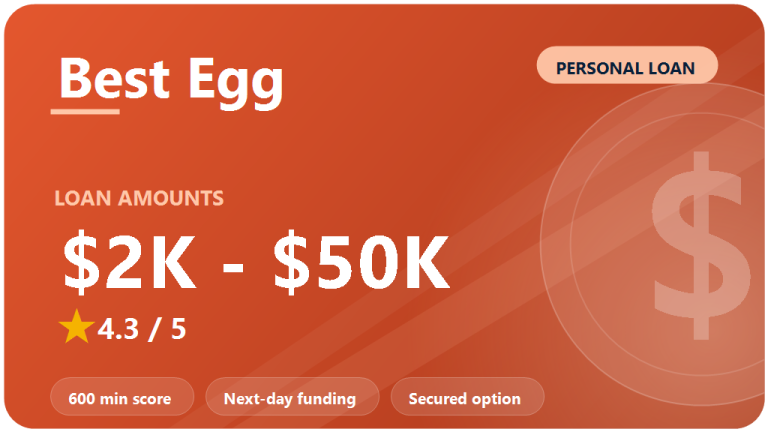

Best Egg Personal Loan Review 2026: Is It Worth It?

Our Best Egg personal loan review covers rates, fees, and funding. Loans from $2,000 with a ~600 minimum score, secured…